What Businesses Need to Know (and Why It Matters)

If your business accepts, processes, or stores credit card information—even just once—you are required to meet PCI compliance standards. But many business owners still ask: What is PCI compliance, and why does it matter to my company?

Whether you’re running a retail store in Colorado, a veterinary clinic, or an e-commerce site, you are part of the payment card ecosystem. That means your business is a potential target for cybercrime. And the consequences of non-compliance—both financial and reputational—can be devastating.

At Tekkis, we help Colorado businesses understand, achieve, and maintain PCI compliance as part of a broader cybersecurity strategy. In this post, we’ll walk you through what PCI compliance means, who it applies to, and how to protect your organization from unnecessary risk.

TL;DR: PCI Compliance Quick Facts

- PCI compliance is required for any business that accepts or processes credit card payments.

- It’s governed by 12 core data security standards designed to protect cardholder information.

- Non-compliance can lead to major fines, lawsuits, and reputational damage.

- Compliance involves securing networks, limiting access, and using approved payment systems.

- It’s an ongoing process, not a one-time task.

- Working with professionals like Tekkis can help you stay secure and compliant year-round.

What Is PCI Compliance?

PCI compliance refers to following the guidelines set by the Payment Card Industry Data Security Standard (PCI DSS). These standards were created by the PCI Security Standards Council, which includes major credit card brands like Visa, Mastercard, American Express, and Discover.

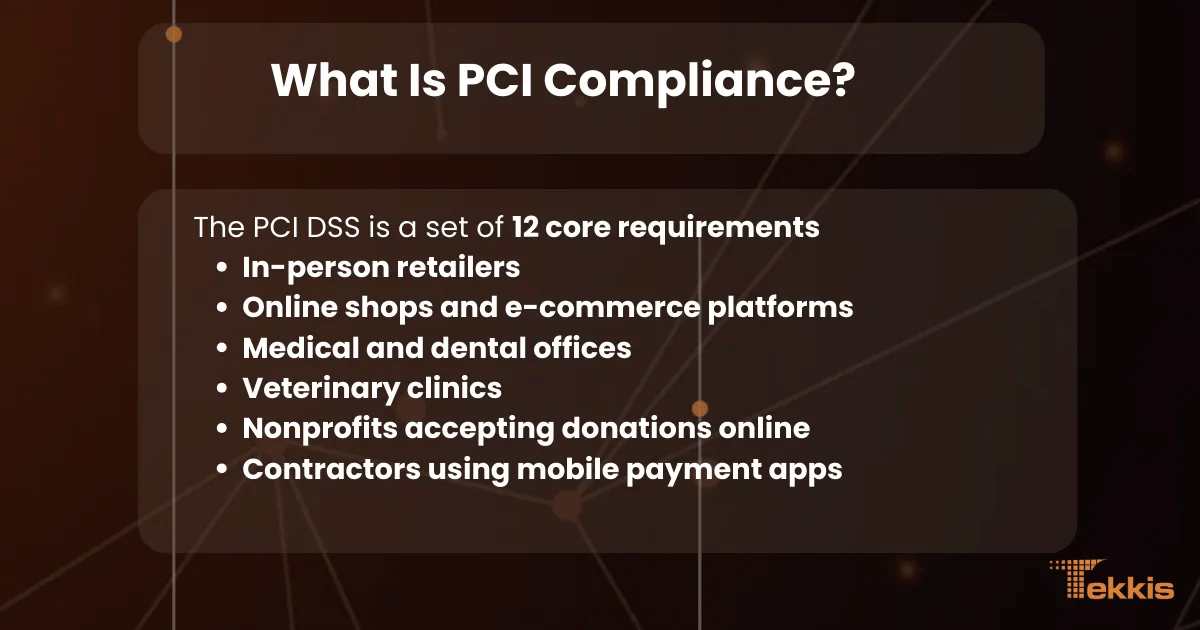

The PCI DSS is a set of 12 core requirements designed to protect cardholder data. These apply to any business—regardless of size or industry—that handles credit card transactions. That includes:

- In-person retailers

- Online shops and e-commerce platforms

- Medical and dental offices

- Veterinary clinics

- Nonprofits accepting donations online

- Contractors using mobile payment apps

Even if you never store cardholder data yourself, if your systems touch that data (e.g., point-of-sale systems, payment forms, etc.), you are responsible for securing it.

Why PCI Compliance Is More Than Just a Checkbox

Too often, business owners see PCI compliance as a regulatory burden—something to check off a to-do list. But compliance isn’t just about avoiding fines. It’s about protecting your customers and your business from real-world threats.

A few examples:

- A single data breach can cost thousands in forensic audits, lawsuits, and lost trust

- You may lose your ability to accept credit cards entirely

- You may be held financially liable for fraudulent transactions that result from your breach

PCI compliance is not optional. It’s a baseline responsibility in the digital economy.

Common Myths About PCI Compliance

Let’s clear up a few common misconceptions:

“We’re too small to be targeted.”

Cybercriminals don’t just go after big companies. Small businesses often have weaker security, making them easier targets.

“We use Stripe/Square, so we’re covered.”

Even if you outsource payment processing, you still have to ensure your environment is secure. That includes the devices, networks, and platforms you use to connect to those processors.

“We passed a scan once—so we’re good forever.”

PCI compliance is an ongoing process, not a one-time audit. You need to maintain good practices and renew your compliance each year.

What Happens If You’re Not PCI Compliant?

Non-compliance can result in serious consequences, such as:

- Hefty fines from banks or card issuers (up to $100,000/month in some cases)

- Forensic investigations at your expense

- Termination of your merchant account, preventing you from processing payments

- Reputational damage that impacts customer trust

In short, the cost of non-compliance far exceeds the investment in proper cybersecurity and compliance planning.

Key Steps Toward Achieving PCI Compliance

So how do you get PCI compliant? Here’s a breakdown of the process.

1. Determine Your Merchant Level

PCI has different requirements based on your transaction volume. Most small businesses fall under Level 3 or 4, but you’ll still need to complete a self-assessment and may be required to conduct network scans.

2. Understand How Data Flows

Map out how credit card data moves through your business—from swipe to storage (if applicable). This helps identify weak points in your systems.

3. Secure Your Network and Devices

Implement firewalls, antivirus software, and network segmentation to isolate cardholder data environments from the rest of your systems.

4. Limit Access

Only authorized users should be able to view or handle cardholder data. Role-based access, strong passwords, and multifactor authentication are critical.

5. Use Approved Payment Solutions

Always use PCI-validated point-of-sale (POS) systems and payment gateways. Avoid DIY setups or unverified platforms.

6. Complete Your SAQ (Self-Assessment Questionnaire)

This form is used to document your compliance. The version you use depends on how your business accepts payments.

7. Run Regular Scans

If your systems touch the internet (which they almost certainly do), you’ll need to run quarterly vulnerability scans from an approved scanning vendor (ASV).

8. Partner with a Qualified Provider

Working with IT experts like Tekkis ensures your compliance is thorough—not just surface-level.

PCI Compliance as Part of a Bigger Cybersecurity Picture

PCI is just one piece of a secure environment. While it’s mandatory for payment security, businesses should see it as a starting point, not an endpoint.

Aligning PCI with broader frameworks—like HIPAA for medical data or NIST for infrastructure security—can provide layered protection and increase overall resilience.

Best practices like:

- Regular staff training

- Incident response plans

- Continuous monitoring and endpoint protection

...can turn PCI compliance into a competitive advantage, not just a requirement.

Conclusion: Make PCI Compliance a Business Priority

PCI compliance isn’t just about satisfying card issuers or checking a box—it’s about protecting your customers and your reputation. In a time when data breaches make headlines and customer trust is hard-earned, securing your payment systems is a must.

By partnering with experts who understand both IT infrastructure and cybersecurity, you can turn PCI compliance into a strength—not a stressor.

To learn how we help businesses across Colorado meet and maintain PCI standards, visit Tekkis today.

FAQs

What is PCI compliance, in simple terms?

It’s a set of rules that any business must follow to securely accept, process, and store credit card data.

Who needs to be PCI compliant?

Any organization that handles credit card transactions—retailers, medical offices, nonprofits, and more.

What are the penalties for non-compliance?

Fines, legal action, increased transaction fees, or loss of ability to process payments.

Does using Stripe, Square, or PayPal make me compliant?

Not automatically. You still need to secure the devices and networks you use to access those platforms.

How often do I need to renew PCI compliance?

Annually. Most businesses also need to complete quarterly scans to maintain active compliance.